Tokenised Treasury bills are on-chain tokens that give exposure to short-term US government debt through a legal wrapper, fund, trust, note or similar structure. They matter because they bring traditional Treasury exposure into crypto rails, where transfer, settlement and collateral use can become more programmable. But a tokenised Treasury product is not the same thing as holding a Treasury bill directly. The token, issuer, custodian, legal wrapper, blockchain rail and redemption process all add extra layers that beginners need to understand.

What Tokenised Treasury Bills Actually Are

Treasury bills are short-term US government securities. They are normally issued with short maturities and are paid at face value when they mature.

A tokenised Treasury bill product is different from holding a Treasury bill directly. In most cases, the holder owns a token linked to a legal wrapper, such as a fund share class, trust, note, special purpose vehicle or similar structure that holds Treasury exposure. The token sits on a blockchain rail, but the underlying claim still depends on off-chain law, custody, reporting and redemption mechanics.

That distinction matters. The underlying asset may be short-dated government paper, but the thing a beginner interacts with is the token wrapper around it.

Why TradFi And Crypto Markets Care About Them

Traditional finance cares about tokenised Treasury products because tokenisation may make administration, transfer and settlement more efficient. It may also support new collateral workflows and lower some operational frictions if the legal and technical design is strong enough.

Crypto markets care because tokenised Treasury exposure can fit more naturally inside wallet-based and on-chain systems than a traditional off-chain holding. That can make the asset easier to move, reference, pledge or integrate inside permissioned digital-market infrastructure.

This does not mean banks are replacing crypto or crypto is replacing banks. It means both sides see practical uses in putting familiar financial assets onto programmable rails.

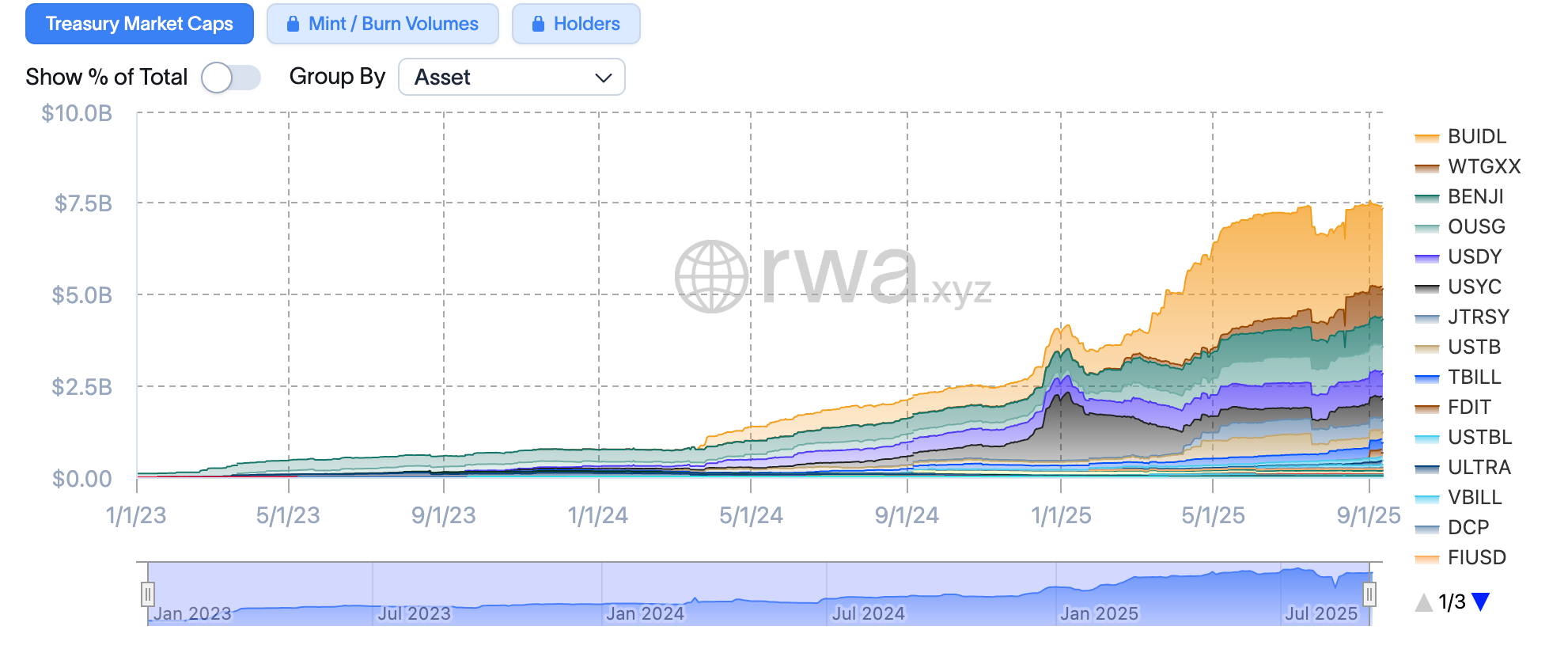

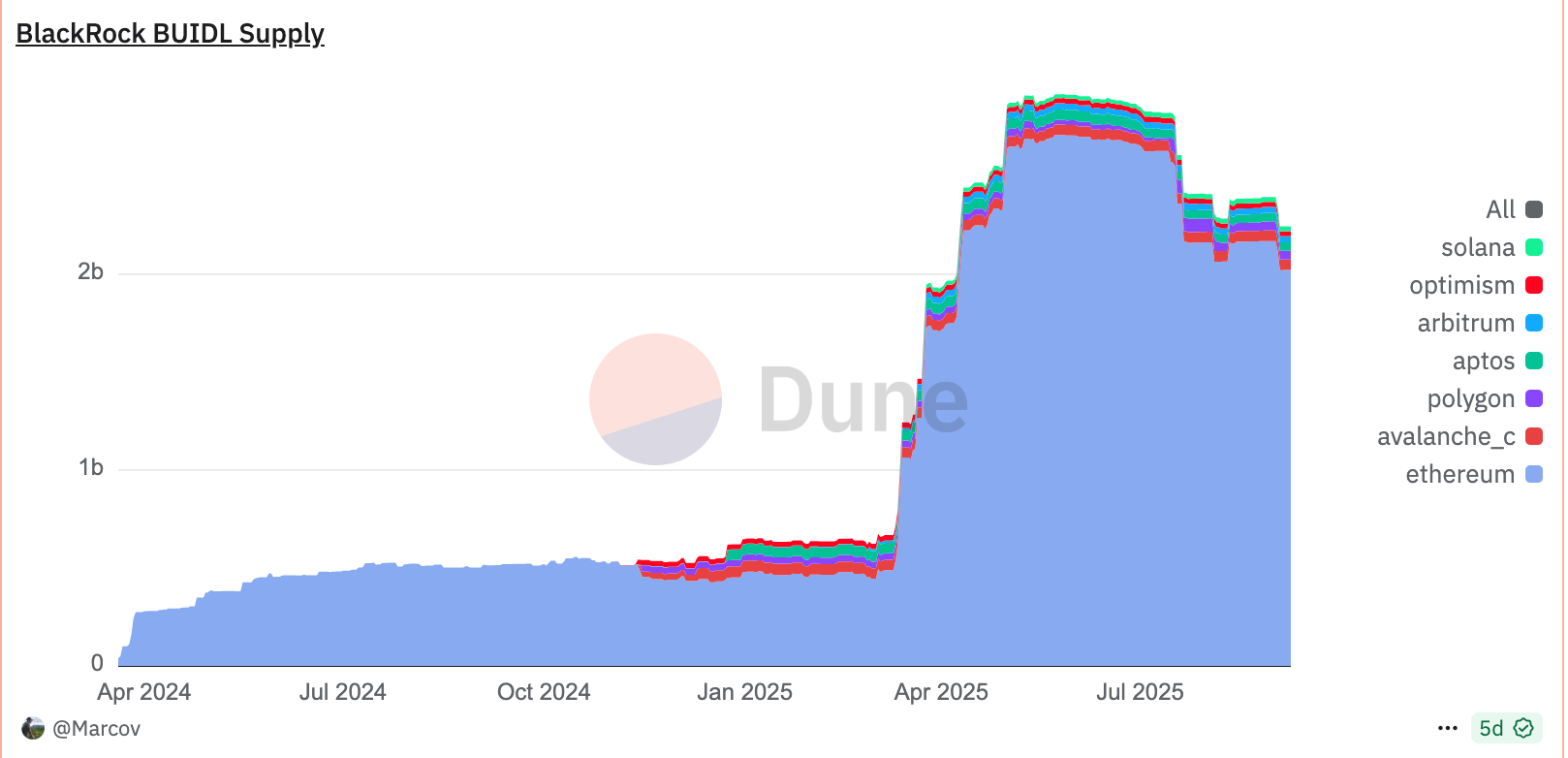

Why BlackRock BUIDL Became A Reference Point

BlackRock’s BUIDL product became one of the clearest reference points for tokenised Treasury exposure because it connected a major traditional finance name with tokenised fund infrastructure. That matters for beginners because it shows the theme is not only a crypto-native experiment.

But the key lesson is still structure. A tokenised fund can make Treasury exposure easier to move through digital rails, but the holder still needs to understand the issuer, the fund design, the custody path, the blockchain networks, the transfer rules and the redemption process.

BUIDL is useful as an example of institutional participation. It should not be read as proof that every tokenised Treasury product has the same risk, liquidity or legal profile.

Why A Tokenised T-Bill Is Not The Same As Holding A Treasury Bill Directly

This is the mistake beginners need to avoid.

When someone holds a Treasury bill directly, they hold a specific government security through a traditional account or custody path. When someone holds a tokenised Treasury product, they rely on extra layers between themselves and the underlying exposure. Those layers can include the issuer, legal wrapper, fund structure, custodian, transfer restrictions, blockchain rail and redemption process.

That means the underlying Treasury exposure and the token wrapper should never be treated as the same thing. A beginner should always separate the government paper from the structure that packages it for on-chain use.

How The Wrapper Around The Treasury Exposure Works

Tokenised Treasury products can use different structures, and the structure changes the risk.

One model is a tokenised fund share class, where the token represents exposure through a regulated fund or similar vehicle. Another is a note or receipt structure, where an issuer promises cash flows backed by Treasury exposure. A third is an on-chain vault or wrapper, where the product holds short-dated paper or fund exposure and issues a redeemable token.

Those models may look similar from the outside because the token may appear to represent Treasury yield. But the risk can differ sharply depending on whether the holder owns fund units, relies on a contractual promise from an issuer, or depends on a specific platform redemption process.

| Structure | What The Holder May Depend On | Main Risk Question |

|---|---|---|

| Tokenised fund share | Fund rules, custodian, issuer and transfer process. | Who can hold, transfer and redeem the share? |

| Note or receipt | Issuer promise and legal claim on the backing structure. | What happens if the issuer or wrapper fails? |

| On-chain vault or wrapper | Smart contracts, platform rules and off-chain asset custody. | How strong is the link between token and underlying exposure? |

What Tokenised Treasury Bills Can Help Solve

Tokenised Treasury products can help solve some practical problems, but only in a limited way.

They may make Treasury exposure easier to distribute across digital platforms. They may improve some settlement flows. They may support collateral use in tokenised-market infrastructure. They may also make some forms of reporting and transfer management more programmable.

Those are real reasons the theme exists. They are not reasons to assume the product is safe, liquid or suitable for every holder.

What Tokenised Treasury Bills Cannot Solve

Tokenisation does not make legal risk disappear. It does not remove the need for custody. It does not guarantee instant redemption. It does not guarantee deep secondary liquidity. It does not remove fees, and it does not automatically make a product safer just because the underlying exposure sounds familiar.

The token may move on-chain, but many of the legal and operational dependencies still live off-chain. That is why “on-chain T-bills” should be read as a structure, not as a shortcut.

The Risks Beginners Need To Understand

The cleanest way to assess tokenised Treasury bills is to separate the risk stack.

| Risk Type | What It Means |

|---|---|

| Counterparty risk | You rely on the issuer, trustee, fund manager, platform or wrapper to operate as promised. |

| Custody risk | Someone has to hold the underlying assets and maintain the legal claim correctly. |

| Technology risk | The token depends on code, platform rules, transfers, upgrades and infrastructure. |

| Liquidity risk | The token may not be easy to sell or redeem in stress, even if it looks liquid on-screen. |

| Regulatory risk | The product may operate under one legal framework while being marketed or accessed globally. |

| Redemption risk | You need to know who can redeem, when, in what size, under what rules and into what asset. |

The important point is simple. Tokenised Treasury bills can have conservative underlying exposure while still carrying extra product-level risks.

Why They Sit Inside The Broader RWA Theme

Tokenised Treasury bills sit inside the broader real-world asset, or RWA, theme because they bring an off-chain financial claim onto an on-chain rail.

That does not mean this article needs to become a full RWA guide. Tokenised T-bills are one specific RWA category with one specific risk stack. They are not the whole RWA story.

For beginners, the useful question is narrow. What is the real asset, what is the token wrapper, who controls the claim, and how does redemption work when conditions are not calm?

How Beginners Should Assess Them Calmly

A beginner does not need to master every tokenisation structure. They need a disciplined checklist.

| Question | Why It Matters |

|---|---|

| What exactly is the legal wrapper? | It shows what claim the token holder really has. |

| Who is the issuer or fund operator? | The issuer controls key parts of the product structure. |

| Who holds the underlying paper? | Custody determines whether the backing is properly controlled. |

| How are reports or attestations published? | Transparency matters when a product claims Treasury backing. |

| Who can redeem, and when? | Redemption rules define whether the token can turn back into value under stress. |

| What chain or platform risk is added? | The token rail can introduce risks that do not exist in the underlying Treasury bill. |

Those questions are more useful than any headline about safe yield or traditional finance entering crypto. The calm beginner read is to treat tokenised Treasury bills as layered financial products. The underlying asset may be short-dated government paper, but the token still depends on structure, custody, law, platform design and redemption mechanics.

Source Note

This article uses public reference material from TreasuryDirect on Treasury bills, plus Bank for International Settlements publications on tokenisation and programmable financial infrastructure. Chart visuals are credited separately below each image.

Mini FAQs

Legal And Risk Notice

This article is for educational purposes only and should not be treated as financial, investment, legal, tax or accounting advice. It does not recommend any tokenised Treasury product, issuer, fund, protocol, platform or allocation approach. Treasury exposure can carry market, liquidity, redemption and operational risk, and tokenised wrappers add extra legal, custody, technology and counterparty layers. Always assess the full structure, not just the headline asset.

Discussion